Introduction

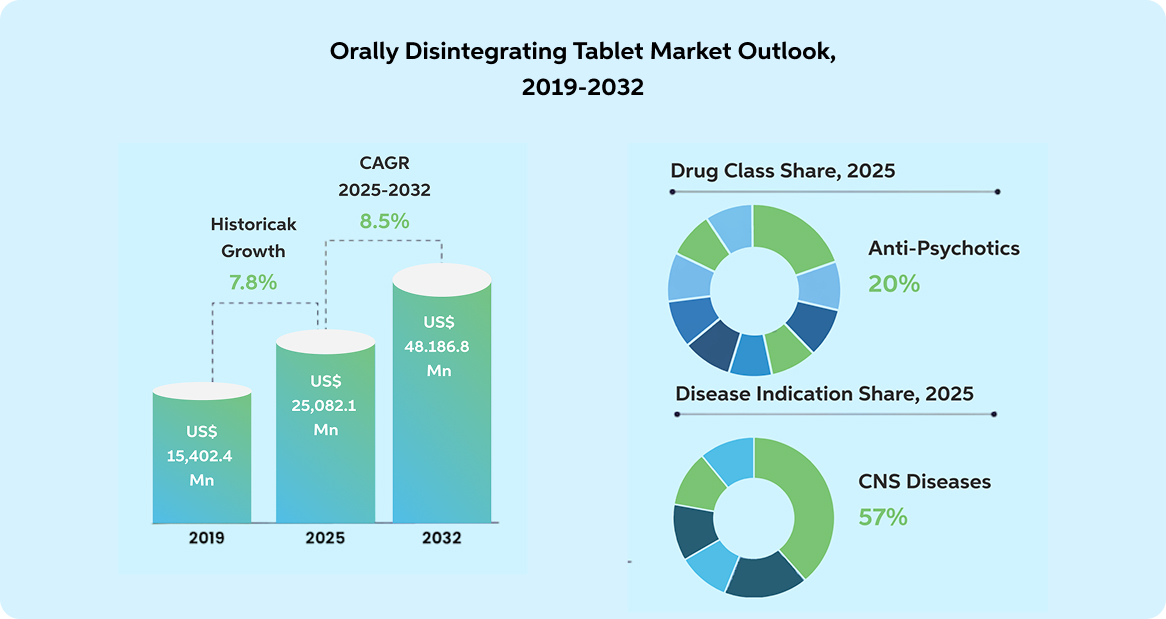

The global orally disintegrating tablet (ODT) market is projected to nearly double from about US$25 billion in 2025 to over US$48 billion by 2032.That surge is pushing ODT platforms into a new role: from patient-friendly dosage forms to strategic assets in portfolio strategy, alongside lifecycle planning, brand differentiation, and supply design.

Reference : https://www.persistencemarketresearch.com/ market-research/orally-disintegrating-tablet-market.asp

This shift changes how scalability is evaluated.

Once an ODT program reaches serious sponsor review, the discussion expands beyond formulation performance. Regulatory, procurement, quality, and commercial teams often evaluate the platform in parallel because the downstream impact is shared.

At this level, scalability ensures delivery reliability across the product journey. Programs that demonstrate end-to-end readiness move faster because they answer operational questions early.

This cross-functional scrutiny is especially evident in three sponsor groups: generic companies pursuing lifecycle extension, innovators exploring adherence-sensitive therapies, and portfolio teams seeking differentiated delivery approaches without molecule change.

“The ODT platform is making a difference across all three, new products, lifecycle extensions, and differentiated generics, because each segment has a different need it can address,” says Kamal Preet, Vice President – Global Business Development (Europe and Rest of World) at InstaPill.

In each case, the dosage form decision carries commercial weight.

How Buyers Recognize a Scalable Delivery Platform

Experienced buyers rarely ask for a single scalability metric. They look instead for operational proof that the platform behaves predictably under real program conditions.

Regulatory track record is one of the first filters. Delivery platforms that have supported submissions and approvals in regulated markets reduce planning uncertainty. When filing routes, evidence expectations, and fee implications are clearly mapped, internal sponsor alignment happens faster.

Manufacturing consistency is another decisive factor. Sponsors look for evidence of repeatable batch performance across products and runs. A strong execution history suggests process control and transferability, both of which matter more in practice than theoretical scale projections.

Packaging performance also plays a larger role than many expect. ODT dosage forms are often screened early for storage and transport resilience. Protective packaging systems and validated stability performance help address this quickly and remove a common adoption hurdle.

Capacity discussions also tend to separate exploratory platforms from scalable ones. Sponsors increasingly evaluate how production can be allocated across products, how expansion would be handled, and how supply continuity is protected under portfolio growth scenarios.

Economic alignment rounds out buyer evaluation. Incremental cost is judged in context against lifecycle extension potential, patient-segment reach, adherence impact, and competitive positioning. Delivery-platform upgrades that support a clear commercial objective are easier to justify internally.

“There are three main drivers. First is patient-centricity and adherence. Second is incremental innovation, especially for products already in the market. Third is fully digital, regulatory-compliant manufacturing. Science, economics, and compliance are coming together,” says Kamal Preet.

Together, these factors determine whether an ODT platform moves from exploratory dialogue to program commitment.

Where ODT Adoption Is Expanding

Adoption momentum is strongest in therapy areas where the route of administration influences how treatment is actually taken.

CNS therapies are a leading example, with a 40% market share and the largest single-product segment in 2023.

Kamal Preet predicts, “In the coming years, I see strong application in migraine and antipsychotic therapies, areas where swallowing difficulty, episodic dosing, and administration experience really matter in real-world use.”

Pediatric and geriatric care continues to generate steady demand. Dosage forms that reduce swallowing difficulty and taste burden address persistent adherence challenges and caregiver constraints. Hospital pharmacies accounted for roughly 28% of ODT distribution share in 2023,underscoring the role of ODTs in supervised and adherence-critical treatment settings. ODTs are increasingly evaluated as primary options for selected molecules rather than fallback alternatives.

Mature, high-volume categories are also contributing to growth. Where mechanism innovation is limited, delivery innovation becomes a practical differentiation pathway. For established brands in the antiemetic or anti-inflammatory space, ODT conversion can support lifecycle extension while remaining within established safety and efficacy frameworks.

Metabolic and weight-management therapies add a newer dimension. Rapid expansion of GLP-1 class treatments has intensified focus on long-term persistence and administration burden. This is prompting earlier exploration of alternative oral and sublingual delivery approaches within pipeline planning.

“ The ODT platform is a globally accepted, patient-centric, commercialisable platform that helps pharma companies turn everyday oral medicines into differentiated, higher-value products, without operational complexity,” she continues.

In the industry, route of administration is becoming a strategic variable in product design rather than a late-stage technical choice.

Delivery Strategy and Brand Strategy Are Converging

Route of administration decisions are increasingly tied to commercial outcomes. Ease of dosing, need for water, taste burden, and administration effort all influence persistence over time. Sponsors are addressing these factors earlier because they affect therapy continuity and brand durability.

ODT dosage forms provide a way to evolve delivery experience without altering pharmacology. That makes them particularly relevant for lifecycle programs and differentiated generics. For portfolio teams, this represents an innovation pathway with clearer regulatory and development boundaries than new molecular entities.

As a result, sponsor diligence is becoming more platform-oriented.

“Companies want to understand what the technology platform delivers scientifically, not only patient convenience. They ask about bioavailability, absorption behavior, and whether we have supporting data,” says Kamal Preet.

Diligence typically centers on a few core questions: Does the platform perform consistently across molecules and at commercial scale? Does it show scientific differentiation? How are absorption and bioavailability affected? Is there clinical evidence to support it?

Delivery strategy is increasingly linked with supply strategy.

What Pharma Leaders Should Be Asking Now

“The first questions are about dispersion time, administration without water, and taste masking. That’s where most technical conversations begin,” says Kamal Preet. “However, serious prospects want to understand what the technology platform actually delivers scientifically, not just the patient-convenience features,” she continues.

As ODT programs gain broader traction, leadership questions are becoming more forward-looking and platform-focused.

Evaluation now extends beyond single-product feasibility toward delivery-platform maturity. Leaders look for evidence of repeatable manufacturing performance, multi-product experience, and predictable process behavior.

Regulatory pathway planning is being addressed earlier. Route-of-administration changes can alter filing requirements and timelines, so early clarity improves program velocity.

Supply strategy is also entering executive review. Sponsors want visibility into expansion pathways, geographic manufacturing presence, and operational resilience. Portfolio ambitions require supply models that can grow with demand.

Economic assessment remains contextual. Incremental cost is weighed against lifecycle extension, adherence impact, market differentiation, and patient-segment expansion. When the delivery strategy supports the commercial strategy, the value equation strengthens.

Packaging and distribution performance now sits within this leadership lens as well.

“One common misconception that companies have is that these tablets won’t survive transportation or packaging stress. Once we showcase the packaging science and the protective structures we use at InstaPill, that concern usually gets resolved,” explains Kamal Preet.

Product integrity through transport and storage is treated as part of platform readiness.

In summary

The broader shift is clear: dosage form and route of administration are becoming strategic portfolio choices. ODT manufacturing is reaching a stage where scalability is measured by regulatory readiness, operational consistency, packaging robustness, and supply commitment across the full lifecycle. And that is when the ODT delivery platform moves from interesting to investable.

Key Takeaways

● Scalability is enterprise-level readiness. Scalability in ODT programs is not just throughput; it’s readiness across regulatory strategy, packaging integrity, CMC controls, CDMO execution, and commercial supply commitments.

● Sponsors evaluate ODT platforms through regulatory track records, manufacturing consistency, packaging robustness, capacity allocation pathways and economics aligned to brand strategy.

● Segments such as CNS, pediatric, and geriatric care where administration experience affects adherence are driving broader adoption and strategic interest in ODTs.

● Buyers increasingly look for scientific proof points, data on absorption, bioavailability, bioequivalence, and clinical outcomes, not just convenience features.

● Pharma leaders are now asking whether delivery strategy supports lifecycle extension, supply continuity, geographic scale, and differentiation, shifting ODTs from tactical to strategic portfolio choices.

References:

- Spherical Insights & Market Research. (n.d.). Orally disintegrating tablet market. SphericalInsights.com. Retrieved January 2026,

- Straits Research. (n.d.). Orally disintegrating tablet market report. StraitsResearch.com. Retrieved January 2026,

- Persistence Market Research. (n.d.). Orally disintegrating tablet market research report. PersistenceMarketResearch.com. Retrieved January 2026,